Basel Committee on Banking Supervision

The Basel Committee on Banking Supervision (BCBS) is an international committee formed to develop standards for banking regulation. As of 2022, it is made up of Central Banks and other banking regulatory authorities from 28 jurisdictions and has 45 members.

The BCBS has developed a series of highly influential policy recommendations known as the Basel Accords. These are not binding and must be adopted by national policymakers in order to be enforced, but they have generally formed the basis of banks' capital requirements in countries represented by the committee and beyond.

Regulatory capital

A capital requirement (also known as regulatory capital) is the amount of capital a bank or other financial institution has to have as required by its financial regulator. This is usually expressed as a capital adequacy ratio of equity as a percentage of risk-weighted assets. These requirements are put into place to ensure that these institutions do not take on excess leverage and risk becoming insolvent.

Under Basel III regulatory capital focuses on high-quality capital, predominantly in the form of shares and retained earnings that can absorb losses.

Total available regulatory capital is the sum of two elements – Tier 1 capital, comprising CET1 and AT1, and Tier 2 capital.

Tier 1 capital

Known as going concern or core capital, Tier 1 is used to fund a financial institution's business activities. It includes Common Equity Tier 1 (CET1) capital and Additional Tier 1 (AT1) capital.

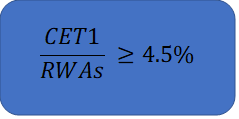

Common Equity Tier 1 capital (CET1):

-

Is the highest quality of regulatory capital, as it absorbs losses immediately when they occurs.

-

Sum of common shares and stock surplus, retained earnings, other comprehensive income, qualifying minority interest and regulatory adjustments

Additional Tier 1 capital (AT1):

Risk-Weighted Assets

RWAs are all assets held by a bank that are weighted by credit risk. Most central banks set formulas for asset risk weights according to the Basel Committee’s guidelines.

The different classes of assets held by banks carry different risk weights and adjusting the assets by their level of risk allows banks to discount lower-risk assets. When calculating the risk-weighted assets of a bank, the assets are first categorized into different classes based on the level of risk and the potential of incurring a loss. The banks’ loan portfolio, along with other assets such as cash and investments, is measured to determine the bank’s overall level of risk. This method is preferred by the Basel Committee because it includes off-balance sheet risks. It also makes it easy to compare banks from different countries around the world.

Riskier assets, such as unsecured loans, carry a higher risk of default and are, therefore, assigned a higher risk weight than assets such as cash and Treasury bills. The higher the amount of risk an asset possesses, the higher the capital adequacy ratio and the capital requirements.

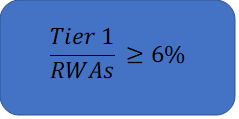

Tier 1 capital ratio

Is the ratio of a bank's Tier 1 capital to its risk. It is expressed as a percentage of a bank's risk-weighted credit exposures. The enforcement of regulated levels of this ratio is intended to protect depositors and promote stability and efficiency of financial systems around the world.

The Basel III agreement, published in 2010, raised the capital requirements. It also introduced the distinction between Tier 1 and Tier 2 capital. Under the new guidelines, the minimum CET1 capital ratio was set at 4.5%, and the minimum Tier 1 capital ratio (CET1 + AT1) was set at 6%.